On April 10, 2026, a three judge panel published an opinion in Morris v. DOJ. In it the Court re-enforced the standing precedent: A tax which does not require a person to pay money to the federal government is not a tax. The precedents cited in the case apply to the cases challenging the constitutionality of the Federal Firearms Act regulation of silencers, short barrelled rifles, short barreled shotguns, and any other weapons. For those items, the tax has been reduced to zero.

The case in the Fifth Circuit is Morris v. DOJ. It is about the ban on home distilleries in federal law, put in place in 1868. The ban does not require a person to pay a tax to produce distilled spirits in the home. Instead, the law prohibits home distilleries altogether. The relevance is there is no tax to be paid. From page 12 of the decision:

“Congress’s authority under the taxing power is limited to requiring an individual to pay money into the Federal Treasury, no more.”

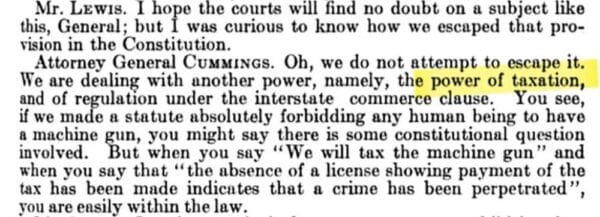

The National Firearms Act (NFA) has always been justified under the authority of the Congress to raise taxes. It has not been justified as authority given to Congress by the interstate commerce clause. This was emphasized by Franklin Delano Roosevelt's Attorney General, Homer Cummings, as shown in a previous article on AmmoLand:

Then-Attorney General Cummings was clear about this in his testimony to Congress during the debates over the bill in 1934:

Courts have consistently upheld the NFA, and its registration provision, on the grounds that it was a tax.

Another Fifth Circuit case is directly challenging the constitutionality of the NFA registration requirements now that there is no tax on silencers, short barreled rifles and short barreled shotguns. Brown v. ATF is at the district court level. Issues of standing are being addressed. If the case proceeds to the question of constitutionality, Morris v. DOJ, the home distillery case would be binding precedent for the NFA zero tax case. Because the home distillery case opinion was filed on April 10, it is possible an appeal to the case will be filed. If an appeal is filed, the case would not have as much precedential value until the appeal is completed.

Analysis: The congressional power to tax was used as a work-around in 1934 to avoid the Second Amendment. The NFA has always been justified as a tax act, not a use of congressional power under the commerce clause. In 1934, the commerce clause had far less reach than it has been given in later years. In 1934, the Supreme Court had yet to rule the power to tax could not be used to subvert the Bill of Rights. In 2026, there is long standing precedent the power to tax cannot be used to destroy the Bill of Rights, and long standing precedent the taxing power has to actually have a tax in order to be legitimate. The NFA tax has been eliminated for silencers, short barreled rifles, short barreled shotguns, and any other weapons. The question is: how long will it take for the Supreme Court to recognize this? This correspondent is not a lawyer. The contents of this article is not legal advise.

©2026 by Dean Weingarten: Permission to share is granted when this notice and link are included.

Gun Watch

No comments:

Post a Comment